🔮 Meaningless Price Path Simulator

What’s the point of this?

This simulator generates random stock paths based on a normal distribution of returns, creating paths that look similar to real stock price movements.

The assumption of a normal distribution for daily returns is wildly inappropriateCont, R. (2000). Empirical properties of asset returns: stylized facts and statistical issues. but that’s more because extreme events are more likely than under a normal distribution. The randomness of price fluctuations themselves in an efficient marketSamuelson, P. A. (1965). Proof that properly anticipated prices fluctuate randomly. Industrial Management Review, 6(2), 41–49. is a pretty reasonable assumption. And that’s the point point: Even if we construct artificial paths that contain no information by definition, they look a lot like real price paths. That means that paths looking like they contain trends of patterns cannot be evidence that they contain information.

See if you can find some paths that—if labelled with a company name—would tempt you to say “this seems like a good investment.” Perhaps you can even spot a “head and shoulders” formation.

Notice how easy it is to see patterns in what is actually random noise – this is called pareidolia, the tendency to perceive meaningful patterns in random data.

Man’s search for meaning

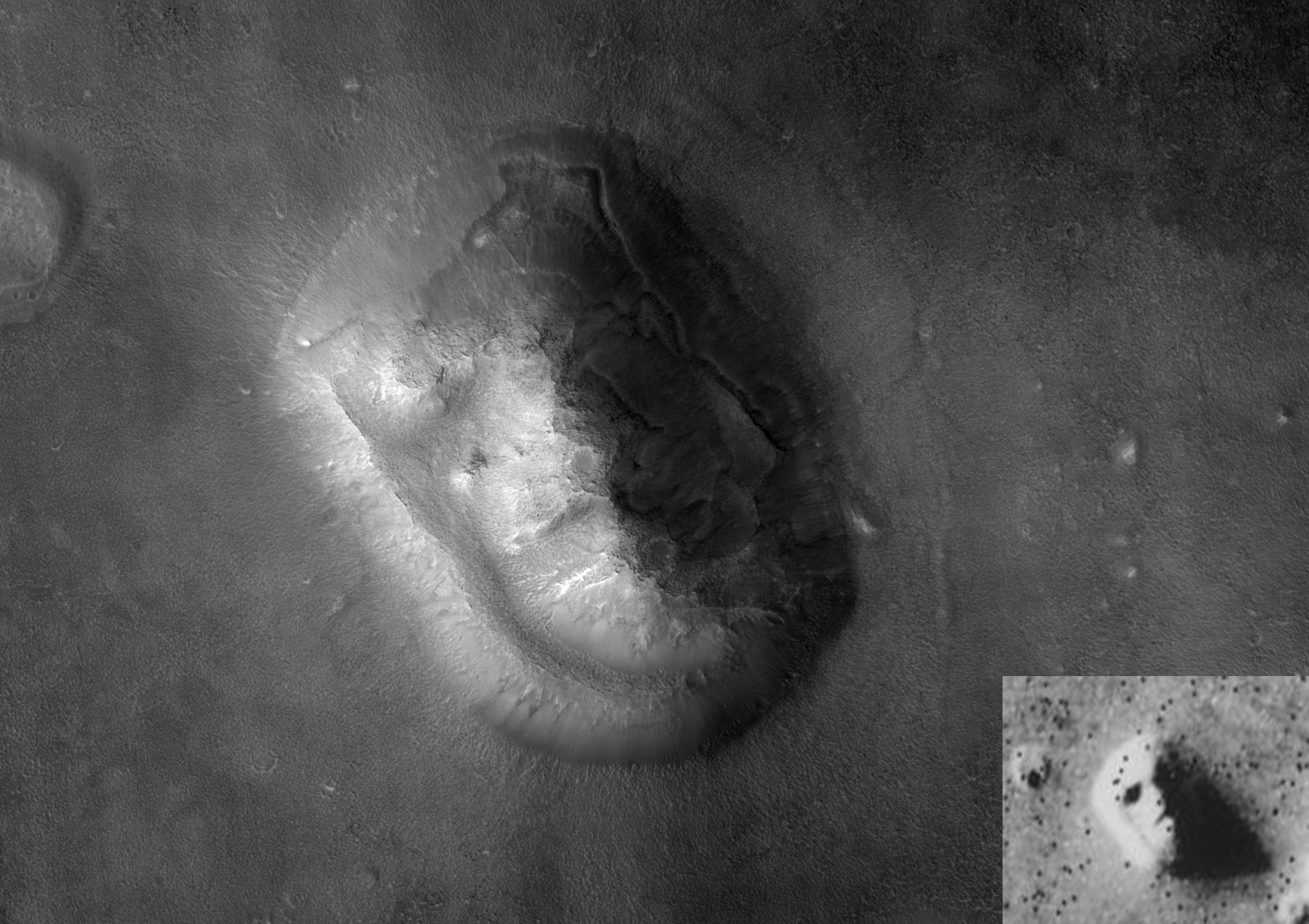

The “Face on Mars” is a famous example of our brain’s tendency to perceive familiar patterns (like faces) in random or ambiguous stimuli.

When first photographed by Viking 1 in 1976, this natural geological formation in the Cydonia region of Mars appeared face-like due to the low resolution and angle of shadows. Higher resolution images later revealed it to be an ordinary mesa. Metaphorically, this is how looking at markets casually is different from looking at them statistically or “at a higher resolution.”

This same psychological phenomenon applies to price and return charts—we instinctively seek patterns and narratives in what are often just random price movements. Just as we might see a face on Mars, traders see “support levels,” “resistance,” and “trends” in what could be merely statistical noise. Add to that a healthy dose of self-attribution biasMiller, D. T., & Ross, M. (1975). Self-serving biases in the attribution of causality: Fact or fiction? Psychological Bulletin, 82(2), 213–225.—the tendency to ascribe successes to our skills and failures to the circumstances—and you can run after noise pretty much indefinitely. Don’t do it.